### Load necessary libraries

# plotting

%matplotlib inline

import pandas as pd

import matplotlib.pyplot as plt

from statsmodels.tsa.seasonal import seasonal_decomposeLoad dataset

fdata = pd.read_csv('./Lab1_Decomposition_v5/Unemployment.dat', delimiter=", ")

fdata.head()/tmp/ipykernel_13141/2043934750.py:1: ParserWarning: Falling back to the 'python' engine because the 'c' engine does not support regex separators (separators > 1 char and different from '\s+' are interpreted as regex); you can avoid this warning by specifying engine='python'.

fdata = pd.read_csv('./Lab1_Decomposition_v5/Unemployment.dat', delimiter=", ")| DATE | TOTAL | |

|---|---|---|

| 0 | 01/01/2010 | 4048493 |

| 1 | 01/02/2010 | 4130625 |

| 2 | 01/03/2010 | 4166613 |

| 3 | 01/04/2010 | 4142425 |

| 4 | 01/05/2010 | 4066202 |

Explore the data

fdata.info()<class 'pandas.core.frame.DataFrame'>

RangeIndex: 156 entries, 0 to 155

Data columns (total 2 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 DATE 156 non-null object

1 TOTAL 156 non-null int64

dtypes: int64(1), object(1)

memory usage: 2.6+ KBMaking the ‘DATE’ column a datetime type

fdata["DATE"] = pd.to_datetime(fdata["DATE"], format="%d/%m/%Y")

fdata.head()| DATE | TOTAL | |

|---|---|---|

| 0 | 2010-01-01 | 4048493 |

| 1 | 2010-02-01 | 4130625 |

| 2 | 2010-03-01 | 4166613 |

| 3 | 2010-04-01 | 4142425 |

| 4 | 2010-05-01 | 4066202 |

fdata.info()<class 'pandas.core.frame.DataFrame'>

RangeIndex: 156 entries, 0 to 155

Data columns (total 2 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 DATE 156 non-null datetime64[ns]

1 TOTAL 156 non-null int64

dtypes: datetime64[ns](1), int64(1)

memory usage: 2.6 KBCreating a Temporal Index

The temporal ordering of the data is so important that it is often used as the index of the dataframe, We can achieve this as follows (MS stands for Month Start):

fdata.set_index('DATE', inplace=True)

fdata.index.freq = 'MS'

fdata.head()| TOTAL | |

|---|---|

| DATE | |

| 2010-01-01 | 4048493 |

| 2010-02-01 | 4130625 |

| 2010-03-01 | 4166613 |

| 2010-04-01 | 4142425 |

| 2010-05-01 | 4066202 |

Silent missing values: time gaps in the data

The following issue we are going to address is a particular problem with time series data. As we have said, the temporal structure of the data is essential. This means that the absence of a data point at a certain time is a piece of information in itself. We call this a time gap in the series and it can easily go unnoticed at first sight. But such time gaps can cause problems in the analysis downstream, as some models will simply be unable to handle them. It is important to get in the habit of detecting time gaps and dealing with them.

We can do that by first creating a sequence of time instants with the same frequency as our time series but without time gaps. We call it a full range below. We do this using the pandas function date_range.

We then simply compare that sequence with the index of the time series:

# Find start and end date of the rime series

start_date = fdata.index.min()

end_date = fdata.index.max()

print(start_date, end_date)

# Generate a full range of months

full_range = pd.date_range(start=start_date, end=end_date, freq='MS') # 'MS' ensures month start

full_range[:5], full_range[-5:]2010-01-01 00:00:00 2022-12-01 00:00:00(DatetimeIndex(['2010-01-01', '2010-02-01', '2010-03-01', '2010-04-01',

'2010-05-01'],

dtype='datetime64[ns]', freq='MS'),

DatetimeIndex(['2022-08-01', '2022-09-01', '2022-10-01', '2022-11-01',

'2022-12-01'],

dtype='datetime64[ns]', freq='MS'))If the missing_months variable below is not empty, it means that we have time gaps in the data. In this case there are no time gaps.

missing_months = full_range.difference(fdata.index)

missing_monthsDatetimeIndex([], dtype='datetime64[ns]', freq='MS')If there were time gaps the code below would fill the other variables as missing values (NaN), which we can then deal with later on.

fdata = fdata.reindex(full_range)

fdata.info()<class 'pandas.core.frame.DataFrame'>

DatetimeIndex: 156 entries, 2010-01-01 to 2022-12-01

Freq: MS

Data columns (total 1 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 TOTAL 156 non-null int64

dtypes: int64(1)

memory usage: 2.4 KBWe can now look for the missing values in the TOTAL column.

fdata.isna().sum()TOTAL 0

dtype: int64There are no missing values in this case. Later we will see how to deal with missing values when they do occur.

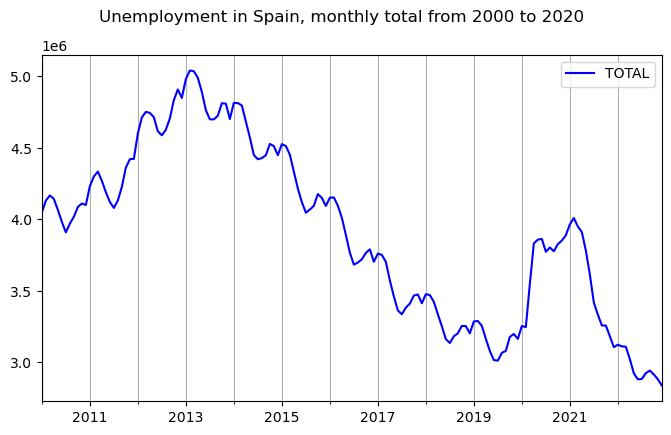

Time plot for the time series:

fig, ax = plt.subplots()

fdata.plot(figsize=(8,4.5), c="blue", ax= ax)

fig.suptitle('Unemployment in Spain, monthly total from 2000 to 2020')

ax.grid(visible=True, which='Both', axis='x')

plt.show();plt.close()

Decomposition methods

fdata| TOTAL | |

|---|---|

| 2010-01-01 | 4048493 |

| 2010-02-01 | 4130625 |

| 2010-03-01 | 4166613 |

| 2010-04-01 | 4142425 |

| 2010-05-01 | 4066202 |

| ... | ... |

| 2022-08-01 | 2924240 |

| 2022-09-01 | 2941919 |

| 2022-10-01 | 2914892 |

| 2022-11-01 | 2881380 |

| 2022-12-01 | 2837653 |

156 rows × 1 columns

This is how to do an additive decomposition:

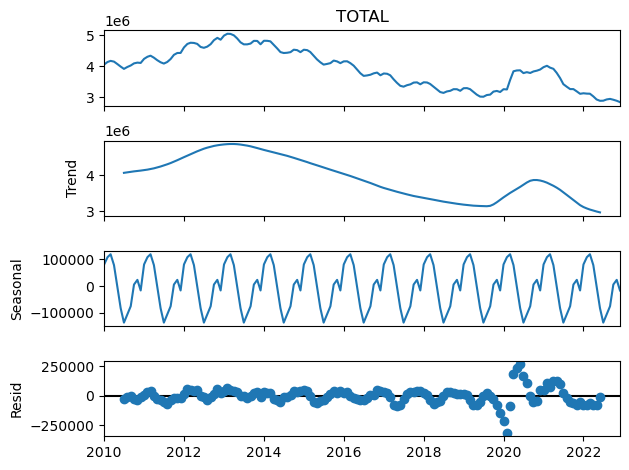

fdata_dcmp_add = seasonal_decompose(fdata['TOTAL'], model='additive')And now we can look at the different components of the decomposition. Beginning with the trend component:

fdata_dcmp_add.trend.head(10)2010-01-01 NaN

2010-02-01 NaN

2010-03-01 NaN

2010-04-01 NaN

2010-05-01 NaN

2010-06-01 NaN

2010-07-01 4.068360e+06

2010-08-01 4.082992e+06

2010-09-01 4.096979e+06

2010-10-01 4.109229e+06

Freq: MS, Name: trend, dtype: float64Note the pure periodicity in the seasonal component. This is a characteristic of this classical decomposition:

fdata_dcmp_add.seasonal.head(24)2010-01-01 80842.168403

2010-02-01 107996.734375

2010-03-01 118956.321181

2010-04-01 78346.404514

2010-05-01 30.897569

2010-06-01 -82320.470486

2010-07-01 -136268.862847

2010-08-01 -105383.043403

2010-09-01 -75046.296875

2010-10-01 5818.828125

2010-11-01 23309.345486

2010-12-01 -16282.026042

2011-01-01 80842.168403

2011-02-01 107996.734375

2011-03-01 118956.321181

2011-04-01 78346.404514

2011-05-01 30.897569

2011-06-01 -82320.470486

2011-07-01 -136268.862847

2011-08-01 -105383.043403

2011-09-01 -75046.296875

2011-10-01 5818.828125

2011-11-01 23309.345486

2011-12-01 -16282.026042

Freq: MS, Name: seasonal, dtype: float64And we can get a nice graphical representation of the decomposition as follows:

plt.figure()

fdata_dcmp_add.plot()

plt.show();plt.close()<Figure size 640x480 with 0 Axes>